The 2 Types of Emergency Funds You Need (and Why They Matter)

Protect yourself from small mishaps and big surprises with this simple savings strategy

An emergency fund is an essential part of your financial toolbelt. This fund is exactly what it sounds like: to be used in the case of emergencies. This can range from unexpected car repairs, house repairs, and more.

It’s recommended that you have anywhere from three to six months' worth of expenses stashed away. This means that if your monthly bills are $4,000 per month, you should have between $12,000 - $24,000 stashed away. This milestone for the mass majority of Americans is likely unreachable, and that’s okay.

That’s why WorkMoney put together a two-part emergency fund that everyone can strive towards. Here’s what you need to know about the two types of emergency funds to strive for.

The Mini-Fund Comes First

Dave Ramsey is famous for his financial baby steps, with the first one being to save $1,000 in an emergency fund. This step is essential to protect you if an unexpected life event occurs, like a car repair or a medical bill. This protects you from having to use a high-interest credit card and potentially ending up in a debt cycle.

The amount of this first fund is up to you, but it would be great to aim for $500-$2,000. Keeping this money in a separate savings account, or even in a secure place at home, can work.

The True Emergency Fund Is Next

Once you have the mini-fund completed, it's time to put the following dollars into the larger emergency fund. This one is meant to cover significant life disruptions, such as illness or job loss.

The general recommendation is to have three to six months of expenses covered in a high-yield savings account. A high-yield savings account is slightly different from a traditional savings account, where the former rewards you with a competitive interest rate, while the latter may likely award you nearly zero.

A high-yield saving account still allows you to have funds quickly accessible, and you’re earning interest along the way. If you do need to dip into the account at some point, once you’re back on your feet, it’s ideal to prioritize refilling the fund back to where it was.

More on Emergency Funds

in The Joy of Money Book

Carrie Joy, the CEO of WorkMoney, highlights why an emergency fund is the foundation of financial stability in her new book, The Joy of Money. Learn more

Starting Small: A Plan For Zero-Saved Readers

If you have no money saved at all, there’s no need to panic. The idea of having months of expenses saved up may seem impossible, but there are ways to get there. But let's start small, even getting to $100 saved is an accomplishment worth noting. Here’s how you can get there:

Automate part of your paycheck: If you get paid once every two weeks, try your best to cut $25 per paycheck into a separate account. In two months, you’ll have $100 stashed away.

Take advantage of unexpected money: If you receive any unexpected gifts, tax refunds, or the like, opt to put this money away in your emergency fund rather than spending it.

A Potential Obstacle To Tackle First

For many people, high-interest debt such as credit cards may be the obstacle keeping you from starting an emergency fund. In fact, roughly half of Americans struggle with credit card debt. If this is you, consider the following options:

Use a 0% APR credit card for a balance transfer: If you have debt on a high-interest credit card, you may consider applying for a card with a 0% APR introductory offer. You can roll your debt from your high-interest card, to one with 0% for a specified period of time.

Consolidate debt into a personal loan: If you have several credit cards with revolving balances, a personal loan may be a way to bring all of the debt together seamlessly.

How Government Programs Can Help You Build Your Funds

While the government doesn’t have benefits to fill your savings account directly, it does have programs to help you potentially offset some of your monthly expenses, keeping you from saving.

Here are a few programs to keep in mind that you may qualify for:

SNAP: The Supplemental Nutrition Assistance Program (SNAP) is a federal program that helps millions of Americans get funding for essential food items.

LIHEAP: The Low-Income Home Energy Assistance Program (LIHEAP) helps families with home energy bills, such as water and electricity.

WIC: If you support children under the age of 5, the Women, Infants, and Children (WIC) program can help you pay for formula and other essentials.

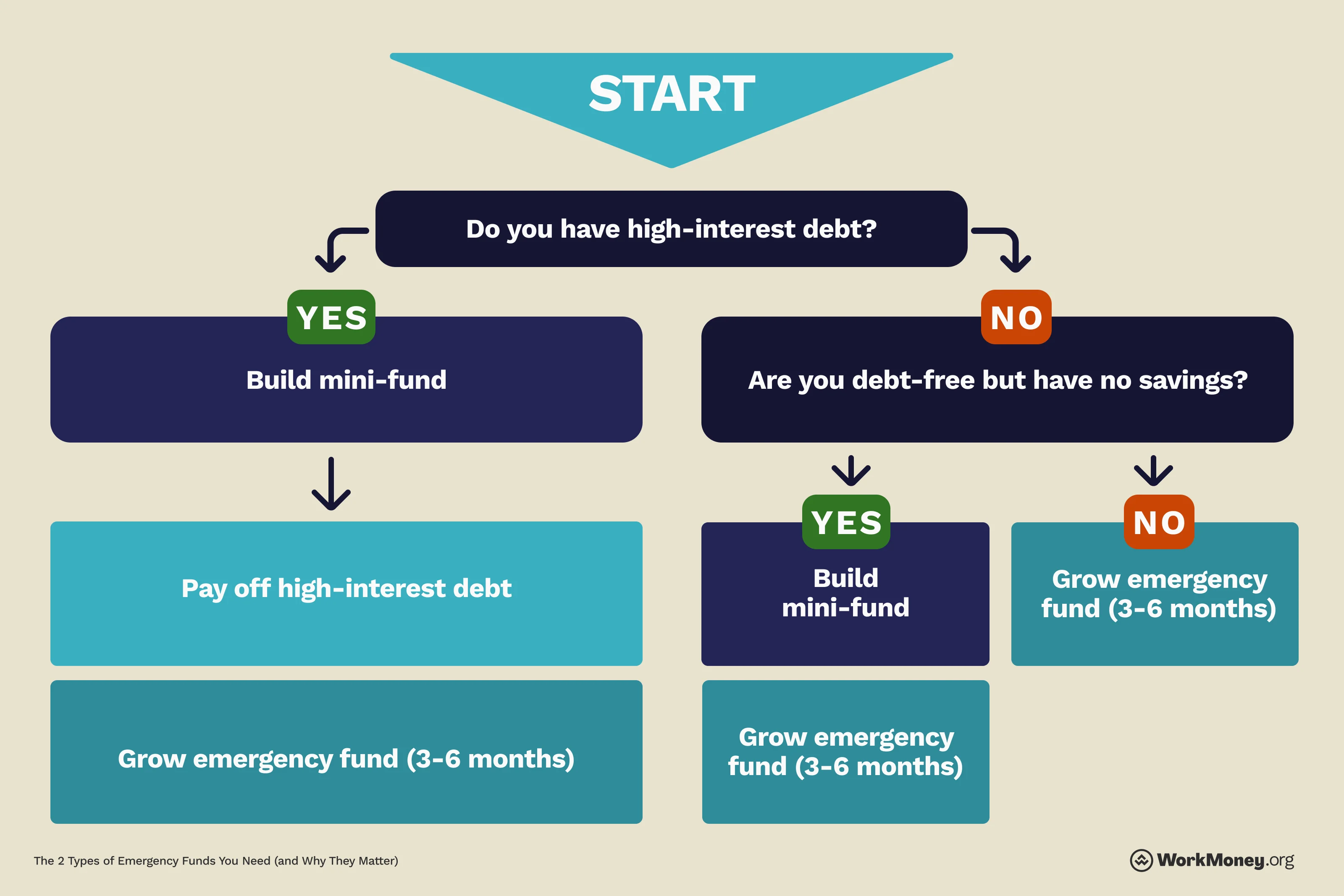

The Fund Flowchart: Which Fund To Build First?

If you’re ready to get started today with saving for the future, here is a simple flowchart.

Do you have high-interest debt (over 10%)? → Yes → Start with Mini-Fund, and then pay off debt

If no, build mini-fund and then emergency fund

Are you debt-free but have no savings? → Build Mini-Fund first.

Once mini-fund is secure → Grow Emergency Fund toward 3–6 months of expenses.

Bottom Line

Money is a significant point of stress for millions of Americans. Two-thirds say personal finances are a significant stressor, according to the American Institute of Stress. However, even if you have high-interest debt, it doesn’t have to hold you back from at least getting started with an emergency fund.

While having a fully-funded emergency fund may not relieve you of all of your financial headaches, it can certainly leave you feeling prepared in case something unexpected happens.

About the Author

Brett Holzhauer

Brett Holzhauer is a Certified Personal Finance Counselor (CPFC) who has reported for outlets like CNBC Select, Forbes Advisor, LendingTree, UpgradedPoints, MoneyGeek and more throughout his career. He is an alum of the Walter Cronkite School of Journalism at Arizona State. When he is not reporting, Brett is likely watching college football or traveling.