Car Repossession Explained: What Happens and What to Do Next

What happens after your car is repossessed and smart next steps

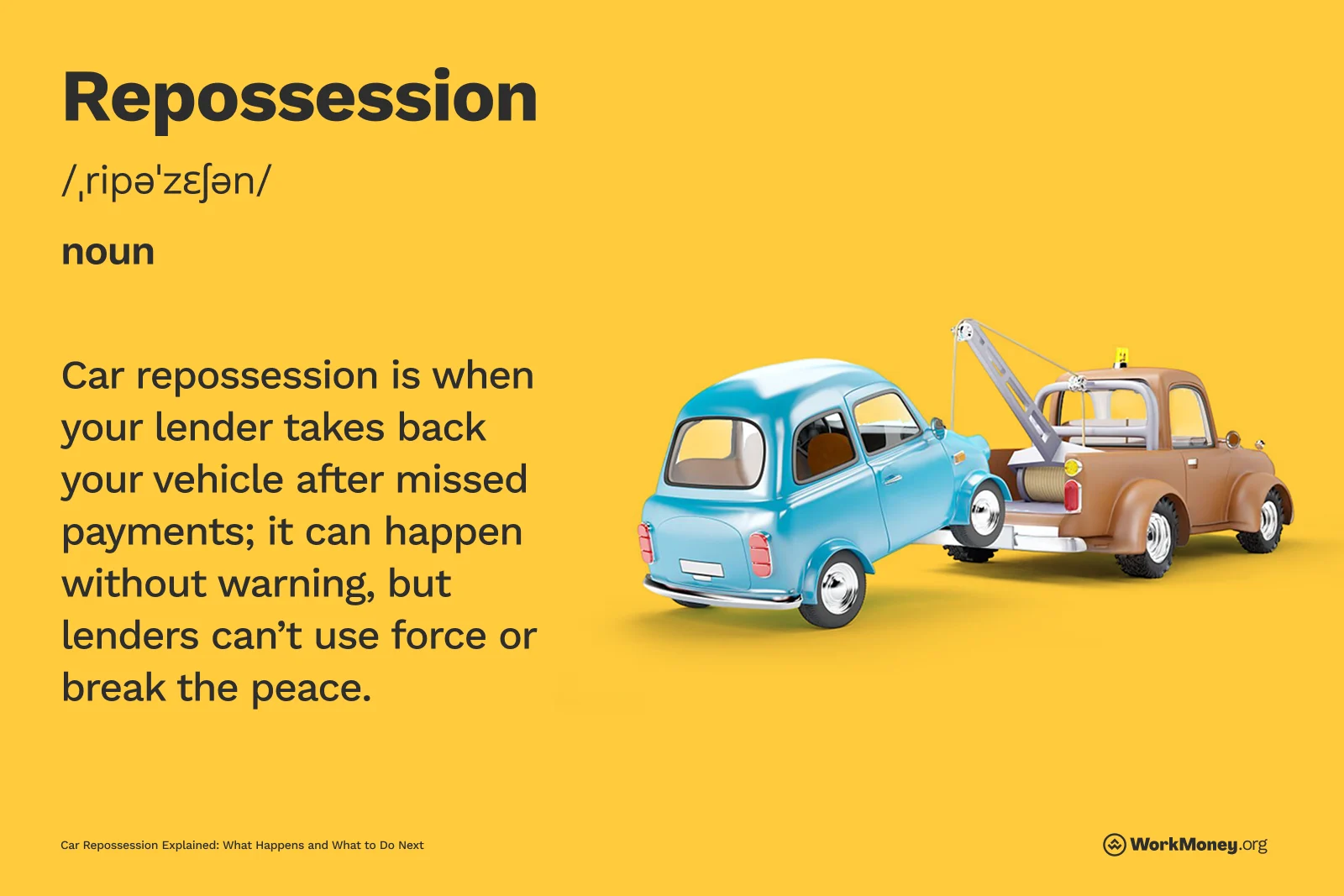

Car repossession is a big deal. If you’ve fallen behind on auto loan payments and default, your lender can take your car. If you’re already tight on money, this might cause you to be out of a vehicle and, in some cases, reliable transportation. Recovering from a car repossession is neither easy nor cheap.

In 2024, there were nearly 1.73 million car repossessions — the highest single-year amount since 2009. The increase in car repossessions indicates a growing number of Americans struggling to make ends meet as basic living costs become increasingly difficult to afford.

If you’re facing a car repossession or you’re already behind on payments and think your car could get repossessed soon, the WorkMoney team shows you how to handle it and what your next steps should be after a car repossession.

Bottom Line

Car repossessions are difficult for anyone who has ever had their car taken away, even if you have a job and you're struggling to make payments. With the rising cost of goods, it’s getting more expensive than ever to pay for all your needs, whether it’s groceries, utility bills, or auto payments.

If you’re on the brink of getting your car repossessed or you think it could happen to you, talk to your lender about restructuring your loan. They would much rather work with you than forcibly take the car from you.

About the Author

Dori Zinn

Dori Zinn is a longtime personal finance journalist with nearly 20 years of experience in digital media. Her work has been featured in the New York Times, Wall Street Journal, CBS News, Yahoo, CNN, USA Today, and more. She loves helping folks learn about money. If she isn’t writing, she’s reading, baking, or watching football.