Does Receiving SNAP Affect Your Credit Score?

Understanding SNAP's impact on your credit and financial stability.

Everyone deserves access to nutritious meals, but stretching every dollar can be challenging. The Supplemental Nutrition Assistance Program (SNAP) helps make buying groceries more affordable, potentially saving you around $199 each month—or even more if you have a bigger household.

When managing their finances, many Americans wonder how government assistance programs, like SNAP affect their credit. The fear that receiving help might damage your credit score is a common worry—but it’s usually based on misunderstandings.

The WorkMoney team is here to explain how SNAP interacts with your credit and share smart financial tips for staying on top of your credit health while benefiting from SNAP.

What Is SNAP?

SNAP is a federal program designed to help millions of Americans afford nutritious food. By providing monthly benefits through an Electronic Benefits Transfer (EBT) card, SNAP puts grocery money directly in the hands of those who need it most. They’re a form of earned support, funded by taxpayers and meant to improve food security for families and individuals across the country.

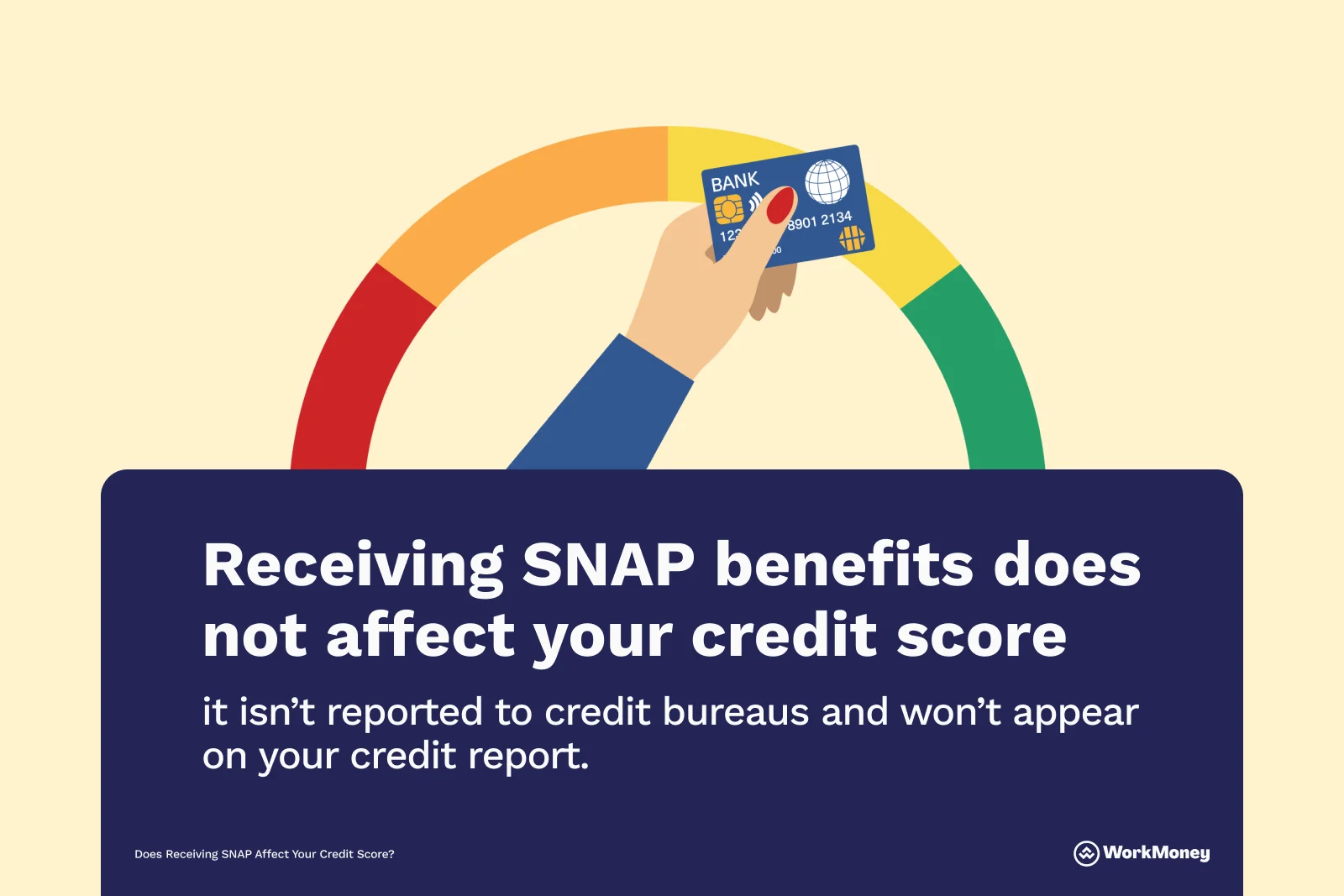

Does Receiving SNAP Affect Your Credit Score?

Unfortunately, misconceptions persist that receiving SNAP could hurt financial reputation or credit scores. This belief that SNAP could harm them financially is a potential deterrent for consumers who need the support the SNAP program offers. The great news is that SNAP benefits don’t affect your credit score.

Credit scores are calculated based on your credit history, which is the record of how you manage debts such as credit cards, loans, mortgages, and other credit accounts. The agencies that calculate credit scores (Equifax, Experian, and TransUnion) rely on lenders to report your financial habits—not on your use of government assistance programs. Receiving SNAP is completely separate from your borrowing and repayment behavior, which means it has no direct effect—positive or negative—on your credit score.

Where the Confusion Stems From

There are a few reasons why some people might worry about SNAP and credit:

Misunderstanding of government benefits: Some people mistakenly believe that any form of public assistance could be reported as debt or cause negative marks on their credit.

Fear of applying for assistance: Consumers may hesitate to apply for SNAP or other programs out of fear that it might “follow them” financially or harm future borrowing.

Financial stress and credit issues coinciding: Often, people who need SNAP benefits are already dealing with tight budgets or credit challenges, so they may link the two incorrectly.

What Affects Your Credit Score?

If you’re worried about keeping your credit score healthy, it’s helpful to understand what a credit score is and how your actions affect it.

Your credit score depends mainly on:

Payment history: Are you paying your credit cards, loans, and bills on time?

Amounts owed: How much of your available credit are you using?

Length of credit history: How long have your credit accounts been open?

New credit: How many new credit accounts or inquiries do you have?

Types of credit: Do you have a mix of credit accounts?

How to Protect and Build Your Credit While Receiving SNAP

Even though SNAP itself doesn’t impact your credit, managing your finances carefully while receiving benefits is key to building or maintaining a strong credit score.

Here are some practical tips that will help you build and maintain a strong credit score:

1. Stay Current on Bills and Credit Payments

Prioritize paying your rent, utilities, phone, and credit cards on time. Payment history makes up the biggest chunk of your credit score.

2. Avoid Payday Loans or High-Interest Borrowing

If you need extra funds beyond SNAP, steer clear of high-interest loans, which can trap you in debt. What’s more, they don’t help your credit score.

3. Monitor Your Credit Reports Regularly

You can get a free copy of your credit report from each of the three major bureaus once per year at AnnualCreditReport.com. Regular checks help you catch errors or fraud early.

4. Consider Credit-Builder Tools

Don’t let all those expensive rent payments go to waste as they can illustrate what a responsible consumer you are. Organizations like Esusu offer rent reporting services that can help build your credit if your rent payments are reported to credit bureaus. On average, users see a +45 point boost in their credit score—without any hidden fees.

The Propel app also supports budgeting and credit-building for SNAP recipients. If you already have SNAP, the Propel app is a helpful tool to maximize your benefits. With Propel, you can easily check your EBT balance, discover exclusive deals, and stay informed about government programs. Sometimes, your initial SNAP amount might be low—like $23 per month—but Propel offers guides to help you submit extra paperwork and potentially increase your benefits. Propel will also help you find which major stores accept SNAP—both in-person and online—so you can shop conveniently and get the best deals.

The Takeaway

Receiving SNAP benefits does not affect your credit score. SNAP is a tool to help with food security, not a loan or debt that lenders track. Clearing up this myth is crucial for those who need help but hesitate due to credit worries.

Remember, your credit score depends on how you manage credit and debt, not on receiving government assistance. Focus on timely payments, managing debt wisely, and using resources designed to support financial health.

You’ve earned the right to access support programs like SNAP—use them confidently as part of your financial toolkit. WorkMoney is here to help you understand these tools, protect your credit, and build a more stable financial future.

About the Author

Jacqueline DeMarco

Jacqueline DeMarco is a seasoned personal finance writer with over seven years of expertise covering important financial topics like credit cards, budgeting, banking, and insurance. Her work has been featured by top financial brands and publications, including Newsweek, Fortune, USA TODAY Blueprint, Bankrate, CreditCards.com, SoFi, and Northwestern Mutual.