The 28/36 Rule: Understanding Debt-to-Income Ratios for Mortgages

Master the math of home buying and learn how to position your finances for a mortgage approval

Buying a home can be an exciting purchase, which can lead some to potentially stretch their budget to the max. This scenario is commonly known as being “house poor.”

To avoid this financial stressor, the 28/36 rule is a solid principle to align on before purchasing a home. The 28 refers to the percentage of maximum gross monthly income that should go to your housing bill (principal, insurance, taxes, and insurance). The 36 represents the maximum percentage that should go to total debt obligations (housing, student debt, credit cards, etc.)

By following this rule, you’ll be able to buy a home that you can comfortably afford. WorkMoney put together a guide to break this down further.

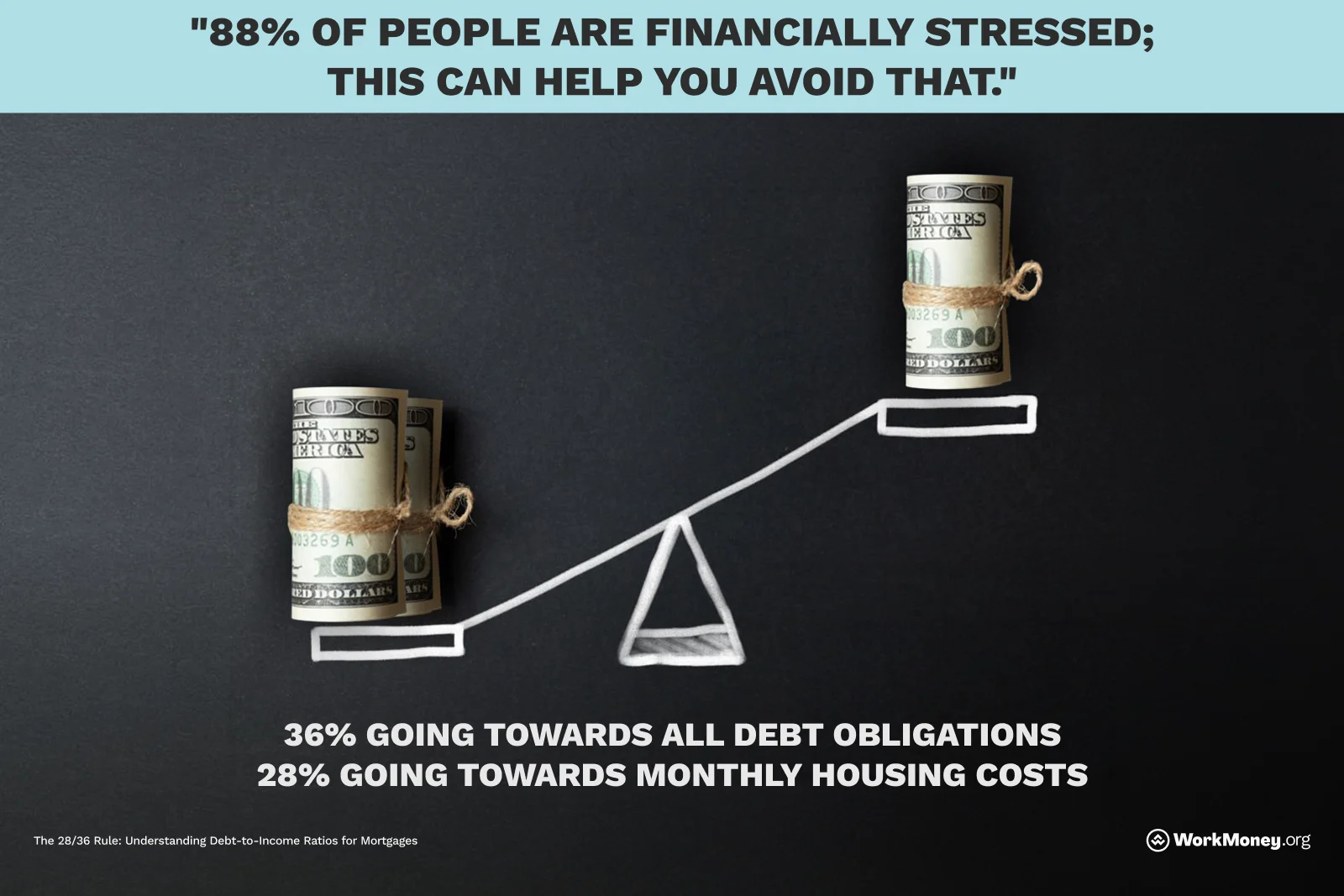

What the 28/36 Rule Means

This rule isn’t meant to be a means of restriction, but rather protection of your financial well-being. Here’s what it looks like for the average household.

The average household has an income of approximately $85,000. This means the following:

28% going towards monthly housing costs = $1,983

36% going towards all debt obligations = $2,550

This leaves $4,500 remaining for their other essential and discretionary spending.

Keep in mind that these numbers are all gross, so before taxes and putting money away for retirement.

The Reality of Ignoring the Rule

This rule is not a requirement to meet in order to purchase a home. However, once the dust has settled and you begin paying down your mortgage, you may feel the sting of your monthly budget. This is called being “house poor”, and it can cause several issues.

Financial stress and anxiety

There’s no question that the majority of people are under financial stress. The latest numbers show that 88% of people surveyed said they felt financial stress to start off the year. Part of that financial stress for homeowners is the post-purchase home repairs and hidden fees, which can cost up to $21,000 per year, according to Bankrate.

With homeownership affordability near all-time lows, it continues to make more sense to rent while you bolster your financial situation.

Healthy vs. Stressed Budgets

Similar to the example above, let's take a family making $90,000 per year. The first family is following the 28/36 rule, while the second family wants to buy a more expensive home.

Category | 28/36 “Healthy” Budget | 45%+ “Stressed” Budget |

Gross Monthly Income | $7,500 | $7,500 |

Housing Costs | $2,100 (28%) | $2,625 (35%) |

Other Debts | $600 | $750 |

Total Debt Payments | $2,700 (36%) | $3,375 (45%) |

Remaining Income (Before Taxes) | $4,800 (64%) | $4,125 (55%) |

Annual Dollars to Debt | $32,400 | $40,500 |

Difference in Annual Debt Load | — | +$8,100 per year |

You can see that the first family has a much lower debt load annually and has significantly more money left over each month.

With this leftover money, the healthy budget family can put more money away for retirement, fill their emergency fund, and have more for discretionary spending each month.

“Path to 36” Checklist: How to Lower Your Debt Ratio

Your debt ratio, commonly known as the debt-to-income (DTI) ratio, is the percentage of what you spend monthly on your debts. This includes a mortgage, student loans, credit cards, car loans, and any other outstanding debt.

Here’s how you can calculate this for yourself: Take your total debt payments and divide them by your total gross income. If the number is larger than 36%, you may find it difficult to be preapproved for a mortgage. At this point, it may be best to aggressively pay down debts before purchasing a home. Here are five ways to get your DTI below the 36% mark:

Pay down high-interest revolving debt first. Credit card balances hit your DTI immediately because lenders use minimum payments in the calculation. Reducing balances (or eliminating a card payment entirely) can quickly lower your ratio.

Increase income before applying. Even a modest income bump from a side hustle meaningfully lowers DTI without cutting lifestyle.

Refinance or restructure existing loans. Extending a car loan term, refinancing student loans, or consolidating debt into a lower monthly payment can reduce your reported monthly obligations.

Avoid new debt 6–12 months before pre-approval. Be sure to freeze your credit and avoid any big purchases during the mortgage prep window.

Lower your target home price. The fastest way to reduce DTI is often to choose a smaller mortgage. A slightly less expensive home can dramatically improve monthly flexibility and long-term financial stability.

Final Thoughts

The 28/36 rule is not meant to be restrictive, but rather avoid financially overextending yourself. As you’re preparing for your home purchase, or you may be in the middle of homeownership, do your best to maintain the 28/36 rule.

Your home shouldn’t be a financial burden, but rather an investment that brings you joy.

About the Author

Brett Holzhauer

Brett Holzhauer is a Certified Personal Finance Counselor (CPFC) who has reported for outlets like CNBC Select, Forbes Advisor, LendingTree, UpgradedPoints, MoneyGeek and more throughout his career. He is an alum of the Walter Cronkite School of Journalism at Arizona State. When he is not reporting, Brett is likely watching college football or traveling.